Regístrese ahora para una mejor cotización personalizada!

By Uwe Lambrette, Director, IBSG Service Provider

By Uwe Lambrette, Director, IBSG Service Provider

Cloud adoption is accelerating at an impressive pace. To gain a deeper understanding of the current rate of change, and the dynamics of cloud's evolution, the Cisco Internet Business Solutions Group (IBSG) engaged with wide-ranging groups of IT executives and decision makers-first in 2010, and then again in 2012. Our in-depth interviews focused on five industry verticals: government, manufacturing, financial services, professional services, and retail.

In our interviews, we encountered many examples of cloud implementation projects, which we call "adoption dynamics," because they are nearly always part of the enterprise cloud adoption process. While there is no prescribed order, enterprises often begin with smaller, well-defined projects that fall into six categories:

Today: Different Industry Verticals Share Common Adoption Dynamics

The studyidentified a number of drivers and inhibitors of cloud adoption, and looked at the ways these play out across different industries. We found that, despite obvious differences among verticals, cloud projects in different industries are bound by the same set of drivers and inhibitors, and can be categorized within the same adoption dynamics. The way cloud adoption plays out may differ because industry-specific business strategies emphasize different key drivers and inhibitors. For instance, for financial services, security and privacy are critical. On the other hand, because manufacturers are dependent on factory legacy systems, they choose different implementation paths, but the triggers for their adoption remain similar to those of financial services.

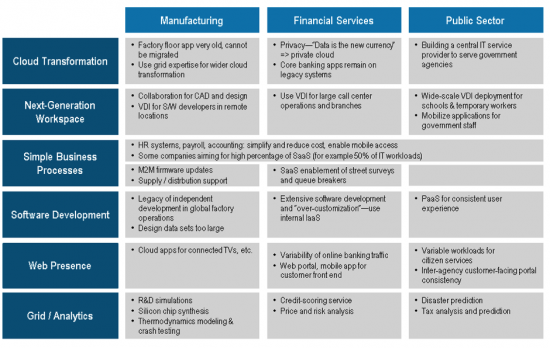

Figure 1. Examples of Industry Projects by Adoption Dynamic and Industry Vertical.

Source: Cisco IBSG, 2012

To underscore this point, Figure 1 highlights industry-specific projects categorized by the six adoption dynamics. Many examples reveal how specific cloud projects in vertical-industry segments are motivated by the same set of drivers and inhibitors:

We also tested the importance of horizontal (not industry-specific) cloud applications. Most enterprise representatives agreed that horizontal workloads (such as email, collaboration, and HR) would migrate to cloud faster than vertical-specific applications. Horizontal workloads have a faster innovation cycle, greater application readiness, and greater scale. Thus, they tend to migrate faster.

Although they are all motivated by similar drivers and inhibitors, every enterprise will make its choice of cloud technologies in the context of its vertical-specific business strategy, and technical solutions will need to link and appeal to business drivers. Cloud service providers, then, need to adapt their go-to-market, sales, and product-bundling strategies to reflect vertical specifics.

The Future: Vertical Cloud Providers

Many interviewees also highlighted the emergence of vertical cloud providers. This is a cloud play for service providers where vertical industry insight is combined with horizontal cloud technologies. Together, these elements provide solutions for key industry challenges, such as smart grid management, health solutions, price management for retailers, or a security life cycle. This can be seen as an extension of the adoption dynamic we call "simple business processes," which to date has focused primarily on horizontal processes, but in the future will also embrace vertical-specific processes.

Several clear implications for service providers emerged from our study:

To learn more, please download our white paper, "Enterprise Journey to the Clouds."

Etiquetas calientes:

nube

Análisis de análisis

IBSG

cloud transformation

Internet Business Solutions Group

grids

adoption

cloud implementation

cloud-based architectures

Etiquetas calientes:

nube

Análisis de análisis

IBSG

cloud transformation

Internet Business Solutions Group

grids

adoption

cloud implementation

cloud-based architectures

Regístrepor correo electrónico ahora para acciones semanales de promoción

100% free, Unsubscribe any time!

Add 1: Room 605 6/F FA YUEN Commercial Building, 75-77 FA YUEN Street, Mongkok KL, HongKong Add 2: Room 405, Building E, MeiDu Building, Gong Shu District, Hangzhou City, Zhejiang Province, China

Whatsapp/Tel: +8618057156223 Tel: 0086 571 86729517 Tel en Hong Kong: 00852 66181601

Correo electrónico: [email protected]

English

English Pусский

Pусский Français

Français Español

Español Português

Português